Paycom Software, Inc. ($PAYC)

“We will remain focused on relentlessly pursuing the best customer service and innovation in the industry.” - Chad Richison

Hello and welcome, if you are not a subscriber, you can do so with the button below:

Originally profiled PAYC 0.00%↑ on April 29 in Four companies to add to your watchlist (2/2) & that was for paid subs but after digging deeper into Paycom I wanted to do a deep dive.

With that out of the way…

What’s inside…

Company (elevator pitch)

About Paycom

Management

Competitors

Financials & Metrics

Risks

Thesis

Conclusion

Holdings Disclosure

Disclaimer is at the end.

1. Company (elevator pitch)

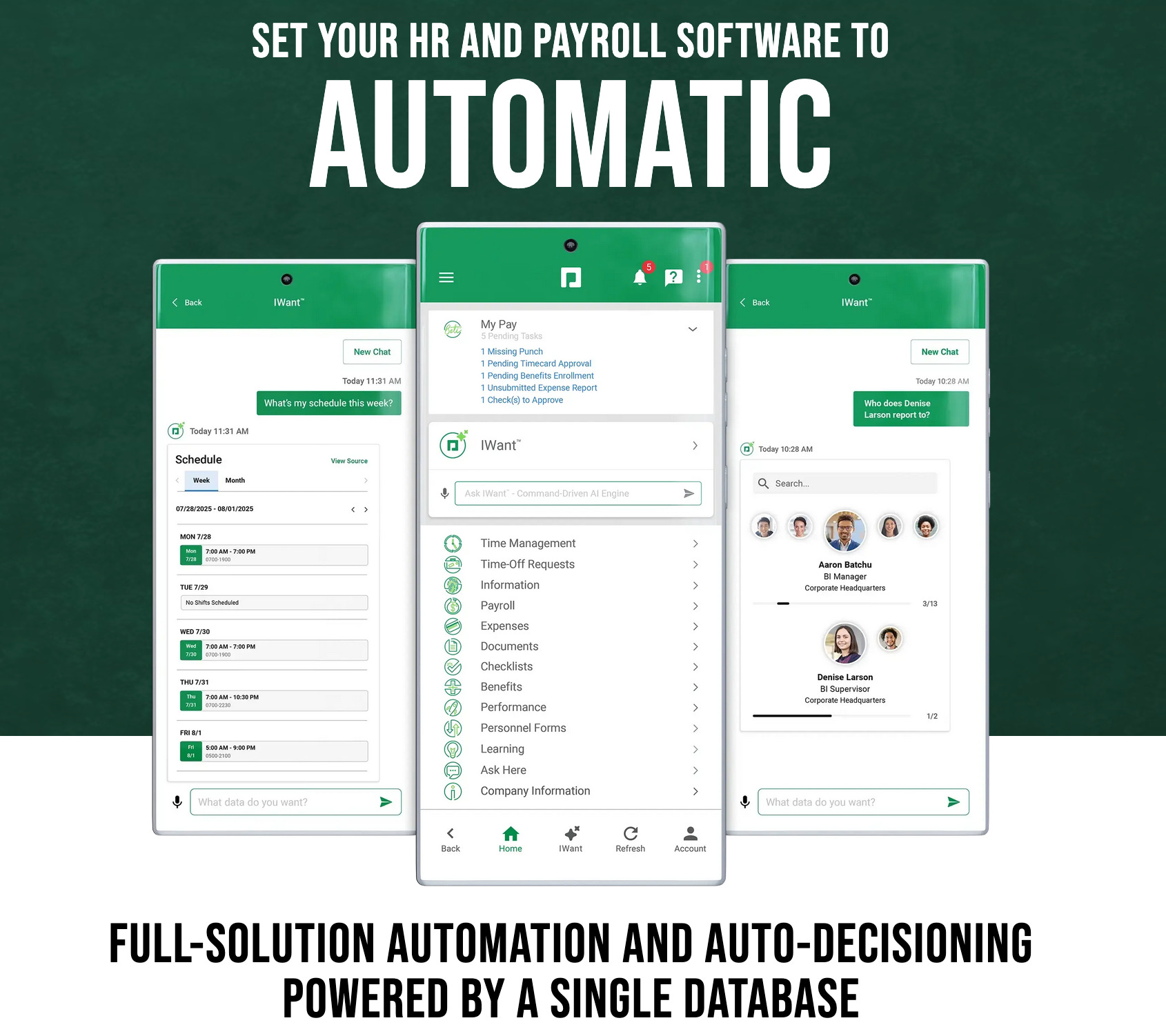

Paycom is a payroll-centric human capital management platform built on a single, unified database that eliminates the need for employers to reconcile multiple HR systems. Its core advantage is its push toward owning and automating payroll workflows—most notably through products like Beti, which shift payroll execution directly to employees.

The investment debate centers on automation. Paycom’s tools can reduce administrative work and improve retention, but they may also cannibalize traditional revenue streams tied to service activity. The bull case is that automation strengthens the moat and re-accelerates growth through better client outcomes while the bear case is that it improves the product without generating enough new demand to offset slowing growth and competitive pressure.

2. About Paycom

Paycom was founded in Oklahoma City in 1998 by Chad Richison. The founding history matters because Paycom was built as a payroll technology company rather than assembled through acquisitions. Richison had prior payroll sales experience, and Paycom’s early insight was that employers wanted payroll to become internet-based, integrated, and less dependent on manual back- office processing.

Since going public in 2014, Paycom’s story has moved through three phases. The first phase was client acquisition and sales-force expansion. The second phase was platform expansion, as the company built payroll-adjacent modules across HR, time, talent, learning, benefits, and compliance. The third phase, and the phase that matters most today, is automation. Paycom is now trying to convince the market that its single database is not merely cleaner architecture, but the foundation for payroll and HR workflows that can increasingly run themselves.

This is why the company talks so aggressively about employee-driven payroll and automation. Paycom does not want to be merely another cloud HCM platform. It wants to own the workflow at the point where the data is created, verified, approved, and corrected. If the employee validates payroll data before payroll is processed, Paycom reduces the need for HR administrators to chase errors after the fact. That is a meaningful change in how payroll work is performed.

What Paycom actually sells:

Paycom sells a cloud-based HCM platform covering the employment lifecycle from recruitment to retirement. In practical terms, that means payroll, tax, time and attendance, talent acquisition, onboarding, HR management, benefits administration, performance, learning, compensation workflows, reporting, and related compliance services. The company’s commercial model is tied to employee headcount, payroll runs, product usage, adopted applications, and recurring platform activity.

Payroll remains the economic center of the platform, but the strategic value is broader than payroll processing. Paycom wants clients to enter employee data once and use it everywhere. The company argues that this reduces duplicate data entry, data conflicts, compliance errors, and administrative labor. In a category where mistakes can be costly and embarrassing, reliability and workflow simplicity matter almost as much as feature count.

There is also seasonality in the model. First-quarter revenue and margins benefit from payroll tax forms, ACA filings, and other year-start compliance activity. Fourth quarter can benefit from bonus payrolls and unscheduled payroll runs. Investors should therefore be careful not to simply annualize the strongest quarter without adjusting for seasonality.

IWant, Beti, GONE, and the automation:

(That was a bit of a play on words, back to serious stuff) Beti is the flagship example of Paycom’s automation strategy. Instead of requiring HR administrators to review and correct payroll after information has moved through the system, Beti pushes payroll verification to employees before payroll is finalized. That sounds simple, but it changes responsibility, timing, and behavior. It reduces the administrative burden on HR, it gives employees direct visibility into their pay, and it can reduce errors before they become exceptions.

GONE extends the same logic into automated time-off decisioning. Rather than forcing managers or HR teams to manually evaluate every time-off request, the system attempts to automate the decision using policy rules and available data. IWant is the AI interface layer that helps users access employee information without navigating the software manually. Together, these tools support Paycom’s larger claim: the company is not adding AI as a marketing feature, it’s trying to remove manual HR work from the process.

The positive is that Paycom has a real workflow advantage. The platform can reduce client labor, reduce errors, and create measurable ROI, so Paycom should have stronger retention, more pricing power, better sales conversion, and better large-client traction. The negative side is that competitors are also adding automation, and that Paycom’s automation may cannibalize work that previously supported revenue. This is something that we need to monitor over the next several years.

3. Management

Paycom is fundamentally a Chad company Chad Richison company. Mr Richison founded Paycom in 1998, has served as CEO since founding, has been on the board since 1998, and became chairman in 2016. As of the 2026 proxy, he beneficially owned about 5.9 million shares, or 12.4% of the company. That is meaningful alignment, and it helps explain why Paycom has maintained a consistent product philosophy for so long.

The executive bench has also been changing. Shane Hadlock became President and Chief Client Officer in February 2026, which aligns with the company’s focus on service quality, client adoption, and automation. Robert D. Foster became CFO in February 2025, bringing payroll and accounting experience. Jeffrey York returned as Chief Sales Officer in January 2026 after previously holding the role for many years. These changes suggest management is trying to tighten the link between product automation, client success, sales execution, and financial discipline.

Board and governance

Paycom’s board has six directors after the resignation of Archana Vemulapalli. The board is classified into three classes, with staggered three-year terms. The board is mostly independent, with five independent directors and one non-independent director, Richison. Frederick C. Peters II serves as lead independent director because Richison is both CEO and chairman. The board brings experience in payments, finance, regulation, technology finance, retail branding, public-company governance, and public policy.

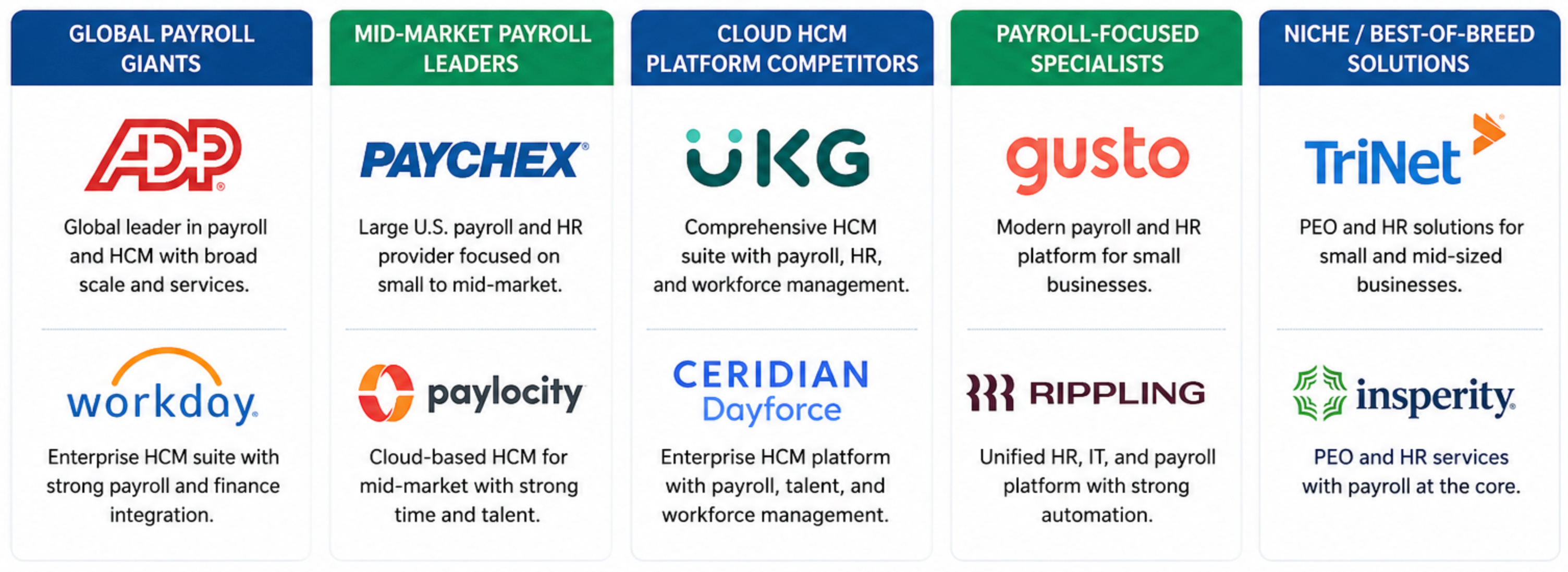

4. Competitors

Paycom competes in a large and highly competitive HCM market. Payroll and HR software is mission- critical because employers must pay employees correctly, withhold taxes, comply with labor rules, track time, administer benefits, and maintain employee records. Switching costs are meaningful because implementation is painful and payroll errors are unacceptable. That is why the best companies in this category can be durable, but it is also why brand, compliance, service quality, and uptime are extremely important.

ADP is the scale incumbent, with global payroll reach, compliance expertise, and a large installed base. Paychex is especially strong among small and midsize businesses. Paylocity is a modern cloud competitor with strong mid-market momentum. Dayforce has deep workforce-management and continuous-payroll capabilities. Workday is stronger in large-enterprise HR and finance. UKG remains a major private competitor in workforce management and HCM. Paycom’s differentiation is strongest when a customer values a unified payroll-first system, less customization, employee-owned data accuracy, and automation that reduces HR workload.

The risk is not that Paycom lacks differentiation. The risk is that competitors can approximate enough of the functionality that customers do not pay a premium for Paycom’s version. ADP can bundle and outspend. Workday can win enterprise relationships. Paylocity can sell a modern cloud experience. Dayforce and UKG can win complex workforce-management use cases.

5. Financials & Metrics

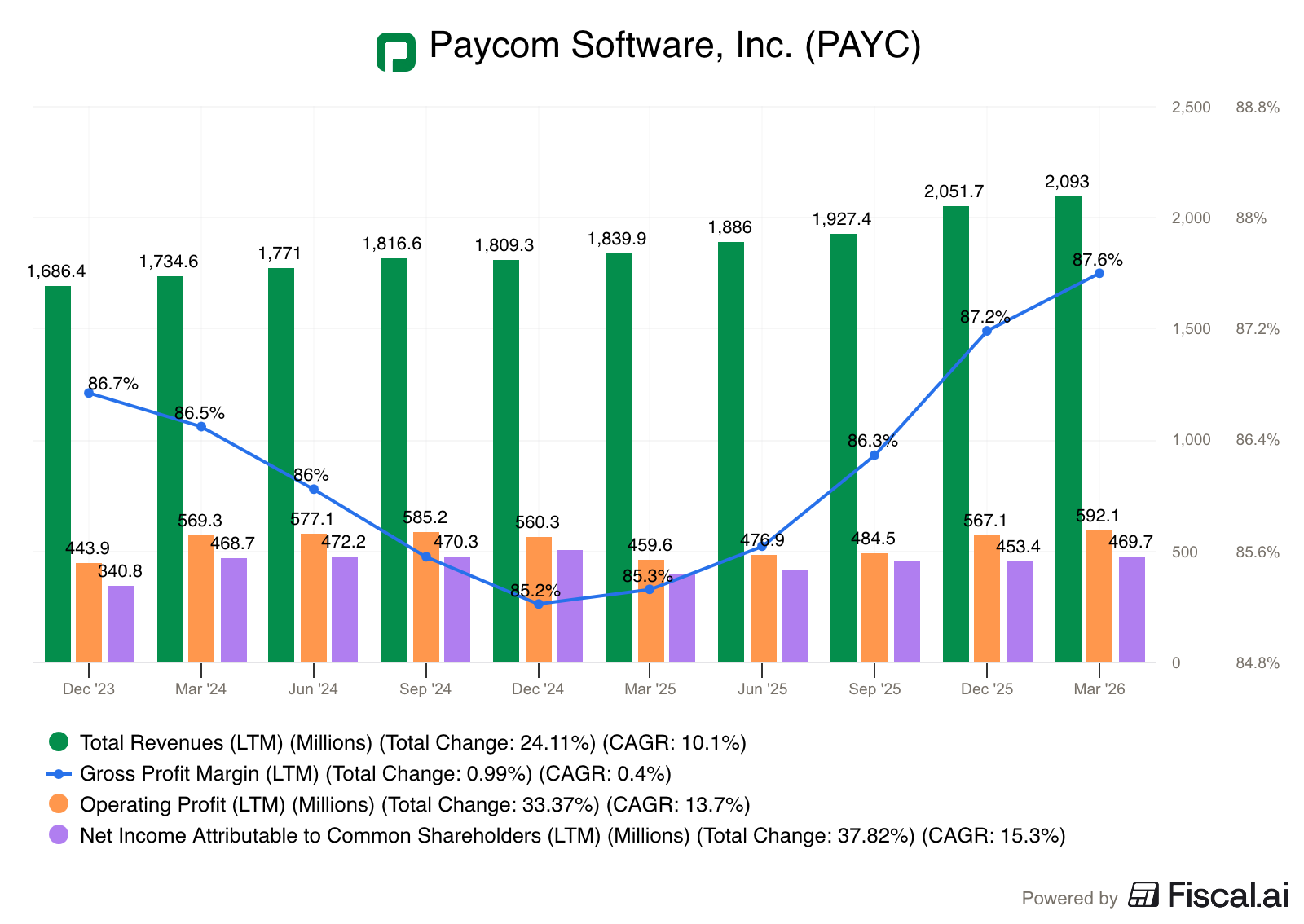

Paycom’s economics are unusually strong for a company whose current growth rate is only mid-single to high-single digits. In 2025, revenue increased 9.0% to $2.052 billion. Gross profit was about $1.706 billion, implying a gross margin of roughly 83.2%. Operating income was $567.2 million, or about 27.6% of revenue. Net income was $453.4 million, or about 22.1% of revenue. This is a highly profitable software and payroll processing business, not a speculative SaaS company burning cash for growth.

The first quarter of 2026 continued the profitability pattern. Revenue was $571.9 million, up 7.8% year over year. GAAP net income was $155.7 million, or 27.2% of revenue. Adjusted EBITDA was $275.4 million, or roughly 48% of revenue. Operating income increased 13.5% year over year, and operating margin improved to 36.8%. The margin performance was excellent; the remaining question is whether revenue growth can re-accelerate.

On one hand Paycom can fund R&D, sales, dividends, and buybacks from a large earnings base, on the other is that company still needs to spend aggressively to compete.

Clients, market penetration, and growth runway

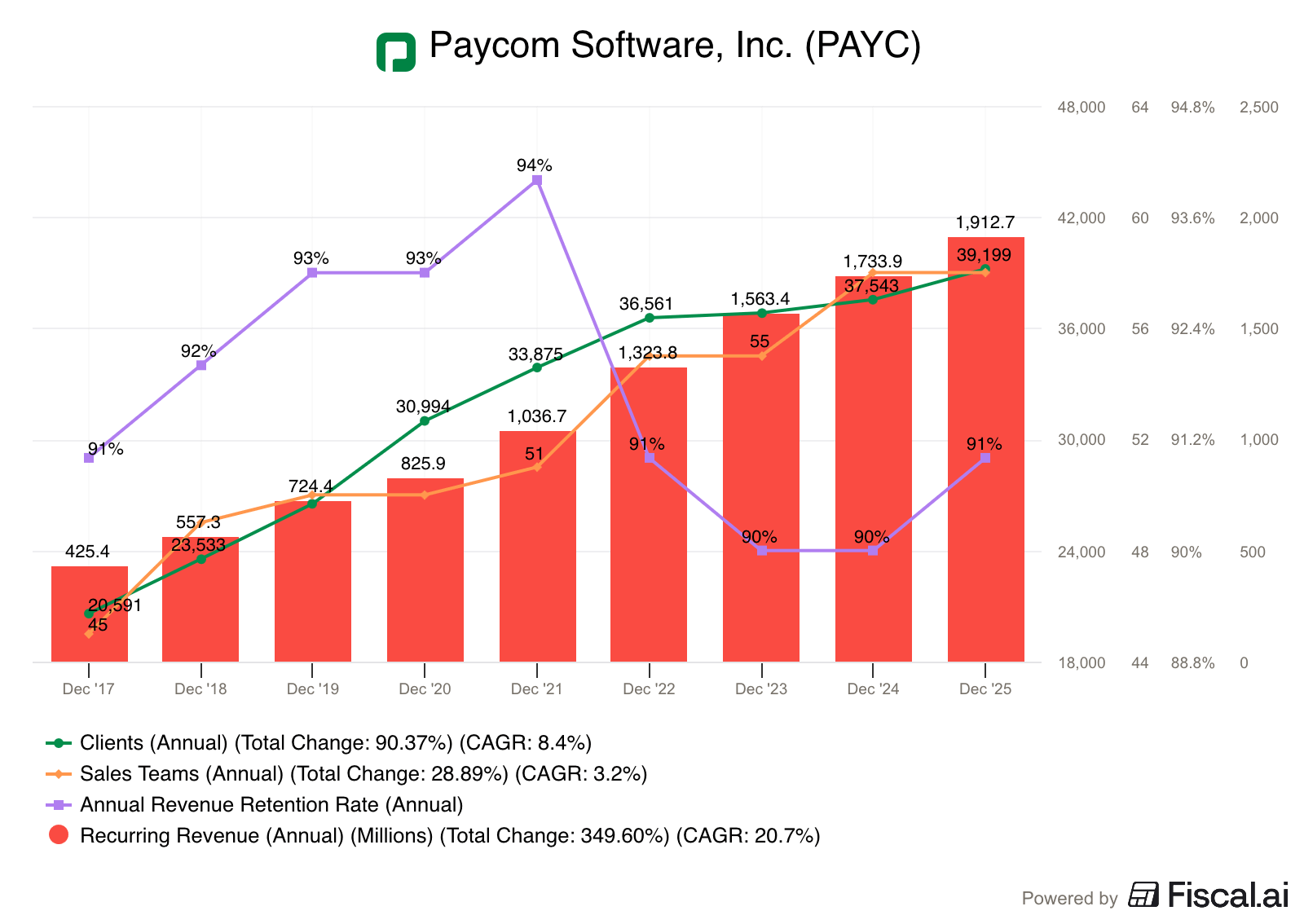

Paycom served about 39,200 clients in 2025, primarily in North America, with a target client size that runs from roughly 50 employees to 10,000 or more. The company still has a meaningful domestic market opportunity, especially if it can win larger employers. Larger clients can produce much more revenue per relationship, and because Paycom’s gross margins are high, incremental revenue from larger clients can be attractive.

The difficulty is that larger clients have longer sales cycles, more complex implementations, more demanding service expectations, and more entrenched existing systems. Paycom’s historically standardized model has worked well in the mid-market. Moving further upmarket raises the reward, but it also raises execution risk. The best evidence that the strategy is working would be higher retention, stronger recurring revenue growth excluding float income, and clear signs of traction among employers with more than 1,000 employees.

Client funds and float income

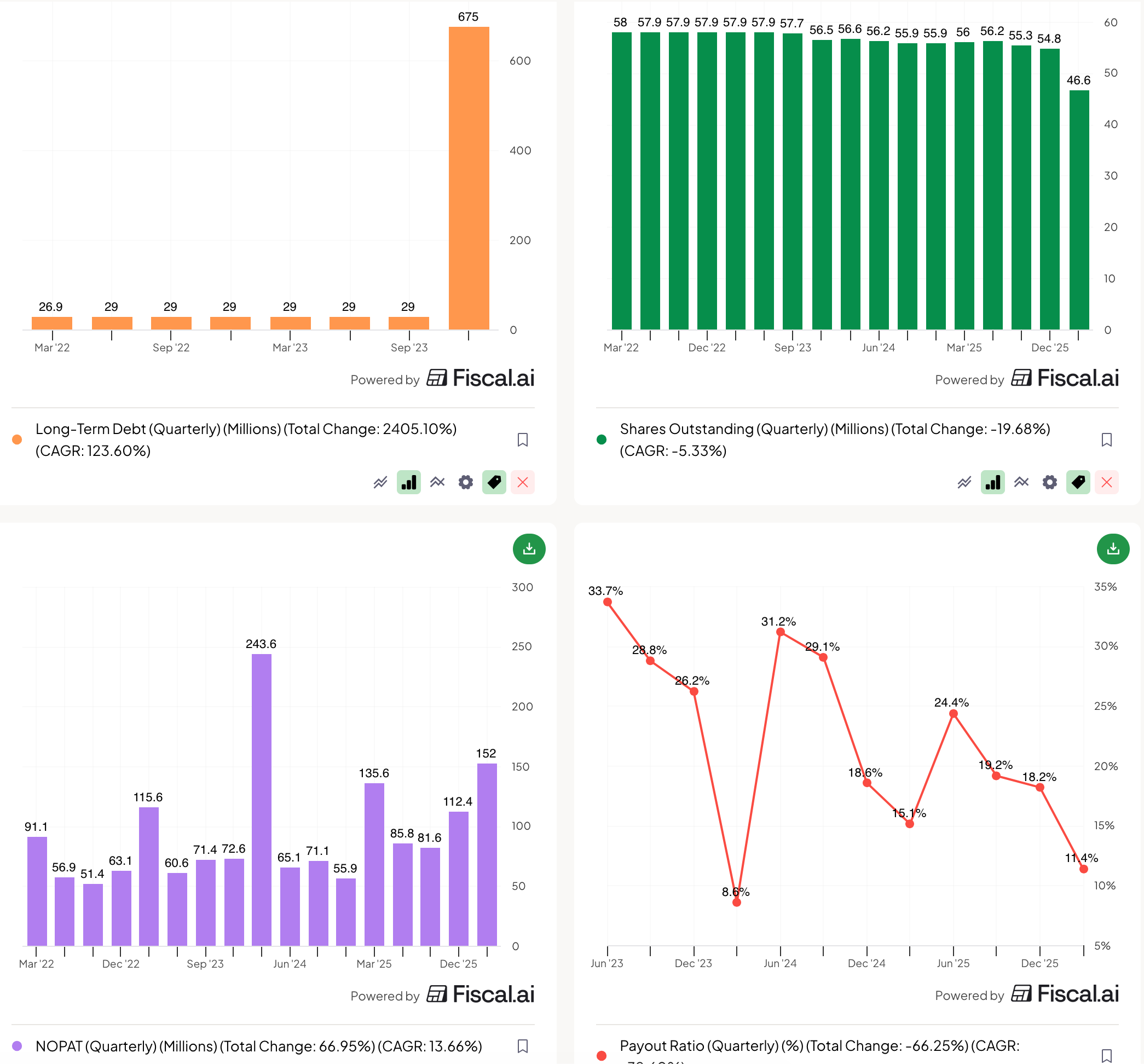

A subtle but important part of Paycom’s model is interest earned on funds held for clients. Payroll processors temporarily hold payroll and tax funds before those funds are remitted to employees or tax authorities. In a higher-rate environment, this float can become meaningful. In 2025, Paycom earned $113 million of interest on client funds. In Q1 2026, interest on client funds was $27.8 million, down from $30.5 million in Q1 2025 even though average daily funds held for clients increased from $2.9 billion to $3.1 billion. The decline came from lower interest rates.

This matters because float income is not the same as recurring software revenue. It can lift revenue and margins when rates are high, but it can also become a headwind when rates fall. Management’s 2026 guidance assumes interest on funds held for clients of about $103 million, down from 2025.

Capital allocation

Capital allocation has become central to the Paycom story. The company pays a dividend and has been aggressive with repurchases. In Q1 2026 alone, Paycom paid $17.7 million in dividends and repurchased 8.375 million shares for about $1.060 billion. That reduced outstanding shares from 54.8 million at year-end 2025 to 46.6 million at March 31, 2026. The company also had $675 million of long-term debt at quarter-end and amended its credit agreement to increase revolving commitments.

6. Risks

Competition is an important risk. Paycom competes against much larger and well-funded companies such as ADP, Paychex, Workday, Dayforce, UKG, Paylocity, and newer HR/payroll platforms like Rippling and Gusto. Paycom’s differentiation is its single-database architecture and employee-driven payroll workflow, but competitors are also investing heavily in automation, AI, self-service tools, and integrated HR suites. If competitors can approximate Paycom’s functionality closely enough, Paycom’s differentiation may narrow and customers may make decisions based more on price, bundled offerings, service levels, or existing vendor relationships.

Paycom is affected by employment, wage activity, interest rates, regulation, and corporate software spending. The labor market matters because Paycom’s revenue is influenced by client employee counts, payroll runs, and employer formation. A stable labor market is usually enough to support payroll activity, while a stronger hiring cycle can help employee counts and client demand. Also interest rates matter through client-funds income, higher rates can support float income while lower rates can reduce it.

Another major risk is that Paycom’s own automation strategy may create longer then expected revenue pressure. Beti, GONE, and IWant are designed to reduce manual work, payroll errors, service needs, and administrative friction for customers. That is good for the client, but it can complicate Paycom’s revenue model. If the platform automates tasks that previously created usage, service activity, or incremental revenue, then the product can become more efficient while reported revenue growth slows.

Finally, capital allocation creates both opportunity and risk. Paycom has been returning capital through dividends and large share repurchases. Buybacks can create significant per-share value if the stock is repurchased below intrinsic value and the business remains durable. But aggressive repurchases are less attractive if growth continues to slow or if the company increases leverage to fund them.

7. Thesis

The base case is that Paycom remains a very good business, but not obviously a premium-growth SaaS compounder. It has a mission-critical product, strong margins, recurring revenue, founder alignment, and a credible automation thesis. It also has slower growth, a competitive market, governance concentration, and uncertainty around how automation changes revenue. The stock can work from the current valuation if earnings are durable and recurring revenue growth excluding float income stabilizes. It can disappoint if growth drifts toward GDP-like levels and repurchases become the main source of per-share growth.

The bull case is that Paycom has a genuine product advantage. The single database, employee-driven payroll, GONE, IWant, and automation tools reduce client workload in ways that competitors cannot easily replicate because many competitors have more fragmented architectures or broader but less unified systems. In that case, the current slowdown is a transition cost. Growth stabilizes and eventually improves, retention moves higher, large-client adoption improves, margins remain strong, and buybacks shrink the share count at attractive prices.

The bear case is that Paycom’s differentiation is real but not commercially powerful enough. Competitors add AI, self-service, and workflow automation quickly. Customers like Paycom, but not enough to offset market maturity, competitive pressure, and automation-related cannibalization. Growth remains in the 5% to 7% range, float income declines, buybacks support EPS but do not create a true growth story, and the company deserves a modest market multiple despite high margins.

A few things that needs to be kept an eye on are:

Recurring and other revenue growth ex interest on clients funds

Annual revenue retention (needs to be 91%+) and clients growth

Products proof of use (Beti, GONE, etc)

Margins durability / debt levels / capital allocation

8. Conclusion

In conclusion, Paycom is not a broken business. It is a financially excellent, founder-led payroll and HCM company with exceptional margins, meaningful ownership alignment, a mission-critical product, and a differentiated automation strategy. The market is asking a fair question: is Paycom’s automation strategy a true growth engine, or is it mainly a retention and margin tool?

The most attractive feature is the combination of profitability, product focus, and founder alignment. The most concerning feature is the possibility that Paycom has already penetrated the easiest part of its market and that future growth requires harder wins against larger and better-resourced competitors. The stock may work well if Paycom grows recurring revenue high-single to low-double digits, holds adjusted EBITDA margins above 40%, and uses buybacks intelligently.

9. Holdings Disclosure

At the time of this publication, I do own shares of PAYC 0.00%↑ in my main portfolio.

P.S. Don’t forget to ❤️ if you enjoyed it.

Disclaimer

The information in this article is provided for informational and educational purposes only.

The information is not intended to be and does not constitute financial advice or any other advice, is general in nature, and is not specific to you. Before using this article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

None of the information in this article is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The author is not responsible for any investment decision made by you. You are responsible for your own investment research and investment decisions.