I go through a lot of companies (that’s how I’m able to pump out BWM on bi weekly basis) and most of them do not meet my investing criteria but once in a while I find a company that I find interesting but that (at that time) might be overvalued and so I put it on my watch list.

I wanted to introduce a bit of different type of “write ups”

I will be sharing four companies, in a short format write ups - two for everyone to see and two for my paid subscribers. All four companies are currently in my IRA account, but none of them are in my main portfolio (yet) … The two behind paywall have priority on my watch-list but I do think all four are interesting and have not been discussed on Substack.

Disclaimer is at the end.

Two industrial and two technology/fintech.

First one is The Gorman-Rupp Company (GRC), I was introduced to it by attending Gabelli’s 36th Annual Pump, Valve, & Water Systems Symposium:

The Gorman-Rupp Company ( GRC 0.00%↑ )

Introduction

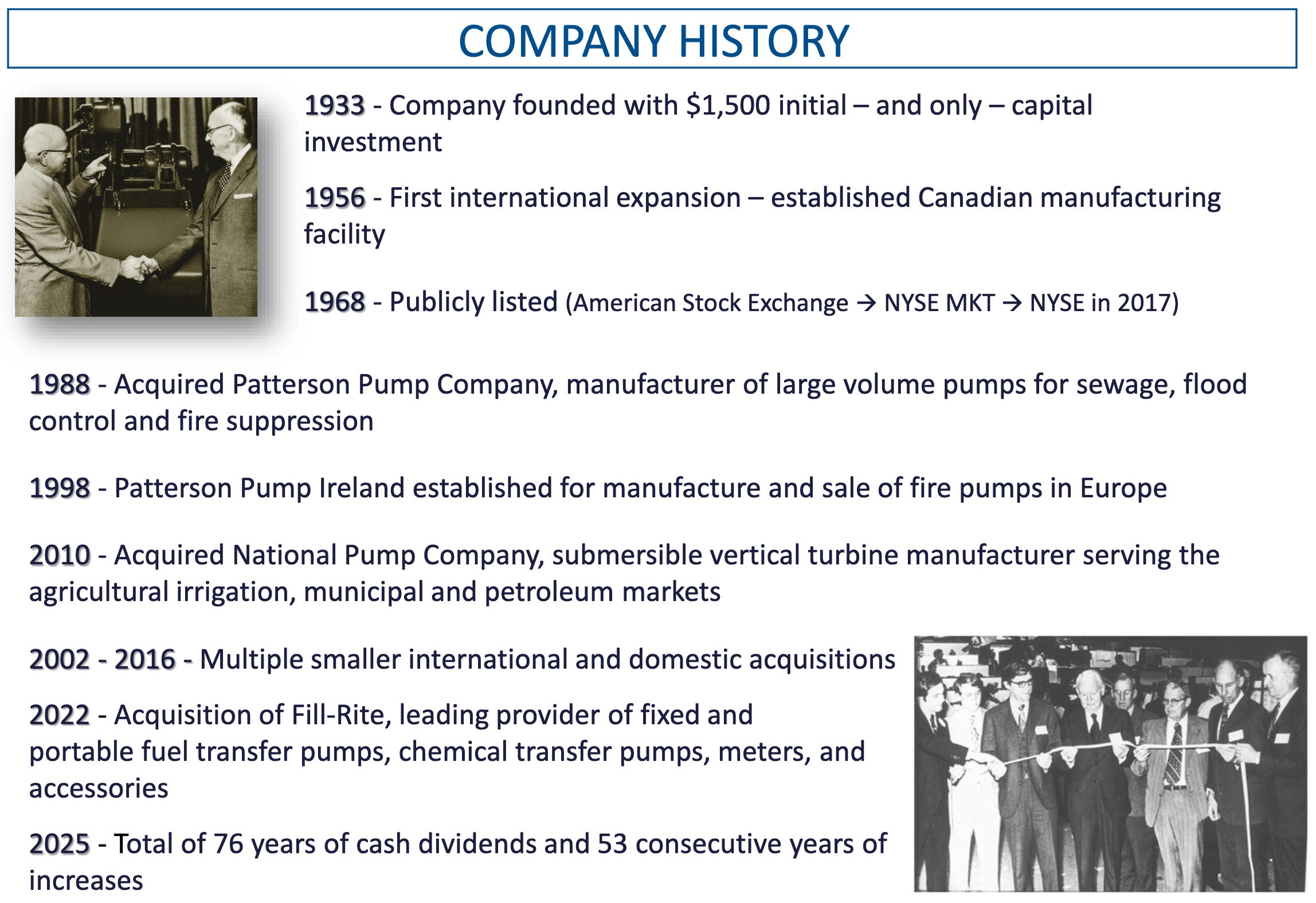

The Gorman-Rupp Company is a long-established industrial manufacturer operating within a highly specialized niche of the global capital goods sector. Founded in 1933 and headquartered in Mansfield, Ohio, the company designs and manufactures pumps and pump systems used in a wide range of mission-critical applications, including water and wastewater handling, fire suppression, industrial processes, agriculture, construction, petroleum transfer, and HVAC systems.

At a high level, Gorman-Rupp resembles a traditional cyclical industrial business. However, a more detailed examination reveals a differentiated model characterized by strong margins, diversified end markets, recurring aftermarket revenue, and disciplined capital allocation. These attributes position the company as a durable industrial compounder rather than a purely cyclical equipment manufacturer.

Business Model and Operations

GRC operates as a single-segment manufacturer of pumps and pump systems, but its operational scope is both broad and technically complex. The company produces thousands of pump configurations ranging from less than one gallon per minute to nearly one million gallons per minute, serving applications that span from small industrial processes to large-scale municipal infrastructure.

A defining characteristic of the business is the application-specific nature of its products. Unlike commoditized equipment, many of GRC’s pumps are engineered solutions designed for specific operating environments. These environments frequently involve demanding conditions and mission-critical functions, such as municipal wastewater systems, fire suppression infrastructure, and industrial chemical processing. As a result, reliability and performance are paramount, and purchasing decisions are often driven by total cost of ownership rather than initial price.

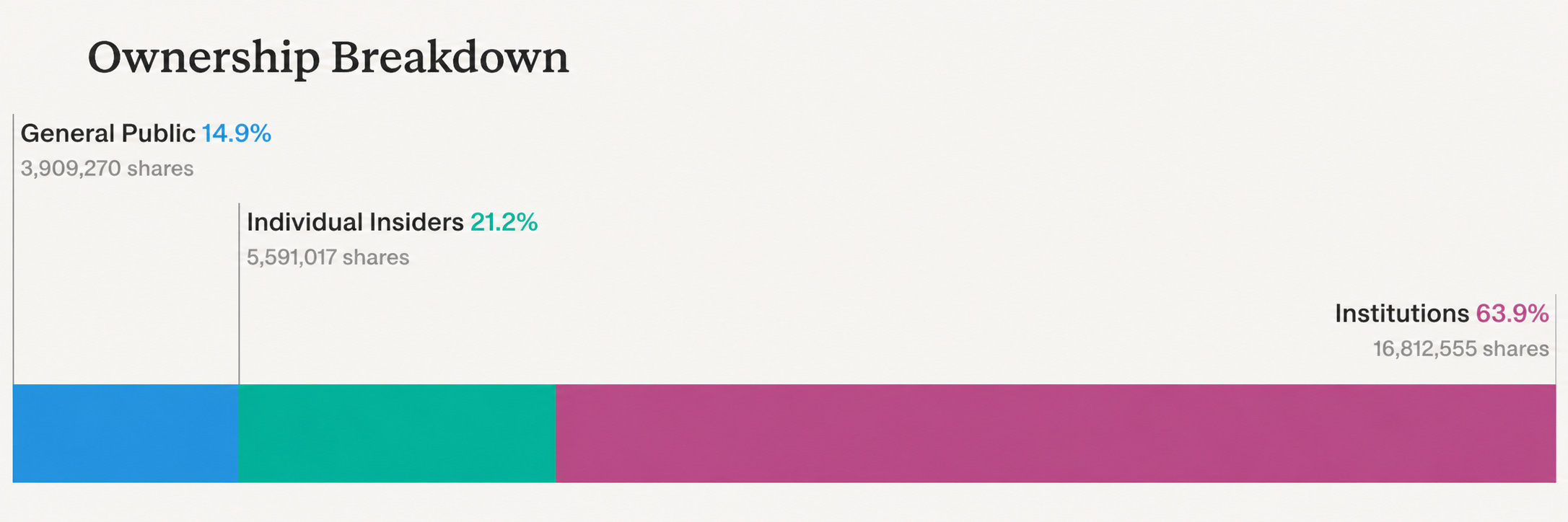

The company distributes its products through a broad network of independent distributors, manufacturers’ representatives, direct sales channels, and international partners. This network enables GRC to serve approximately 140 countries while maintaining localized technical support and customer relationships. Notably, no single customer or country accounts for more than 10% of revenue, reflecting a highly diversified customer base.

Central to the business model is the installed base dynamic. Pumps are long-lived assets that require ongoing maintenance, replacement parts, and eventual replacement. This creates a recurring revenue stream through aftermarket sales, which account for approximately 9% to 12% of total revenue while not contractual in nature, this recurring demand contributes to revenue stability and margin resilience.

Industry Structure and Market Position

The global pump industry is estimated to be approximately $80 billion in annual size and is highly fragmented, consisting of numerous niche-oriented players alongside larger diversified industrial companies. The fragmented nature of the industry is driven by the diversity of applications and the need for specialized engineering solutions.

Within this landscape, GRC competes primarily on performance, reliability, and service, rather than price. Customers in many of its end markets exhibit strong brand loyalty, particularly in applications where equipment failure can result in significant operational or safety consequences. Company’s long-standing reputation for quality and customer service has enabled it to establish durable relationships with distributors and end users.

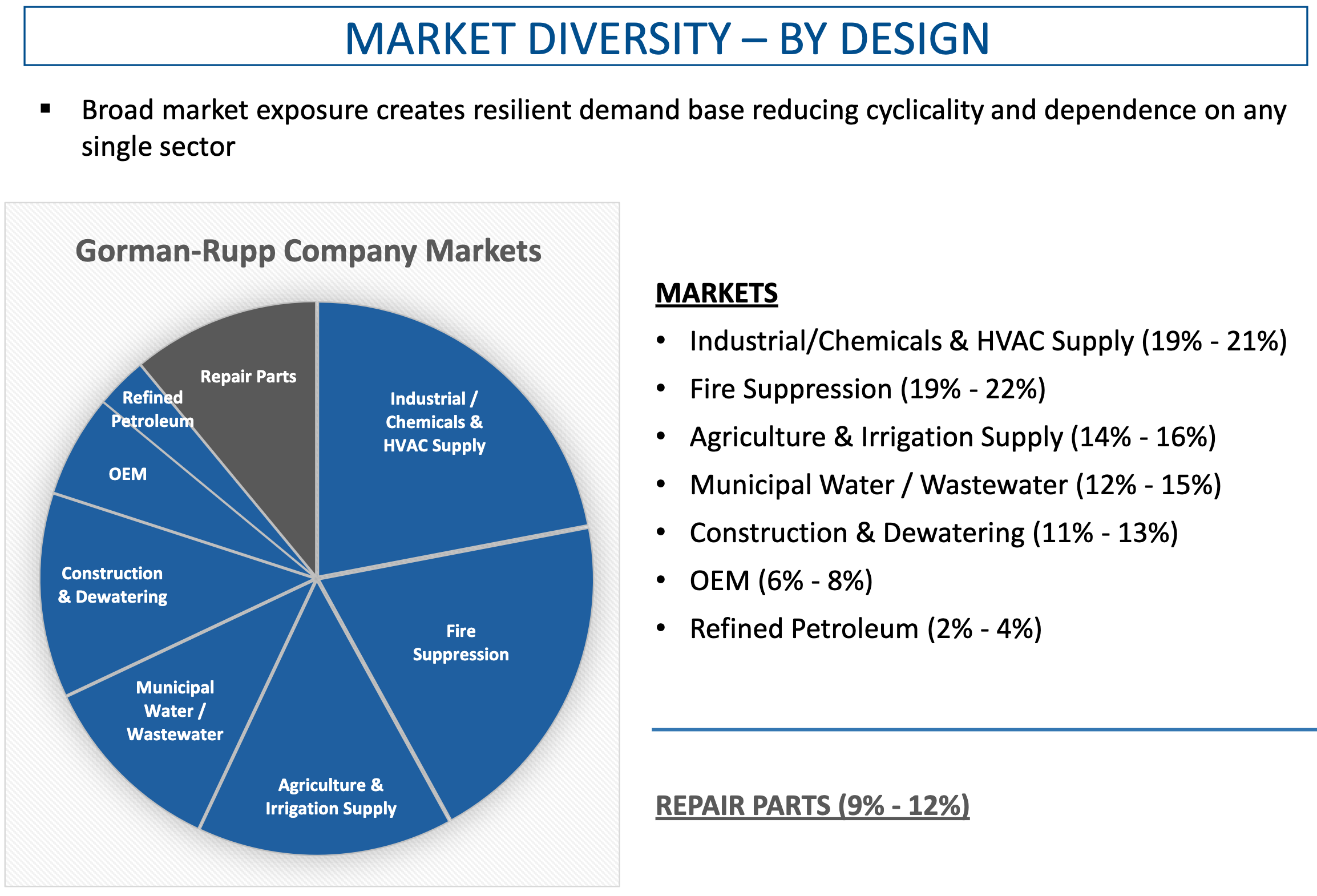

Gorman-Rupp’s revenue is intentionally diversified across multiple end markets, including industrial, fire suppression, agriculture, municipal water, construction, OEM, and petroleum applications.

This diversification reduces exposure to any single economic cycle and allows the company to balance cyclical and non-cyclical demand drivers. While segments such as construction and agriculture are sensitive to economic conditions, others such as municipal water infrastructure and fire suppression are supported by long-term structural demand. The inclusion of aftermarket repair parts further enhances stability.

Management

The leadership of The GRC reflects a deeply operational and internally developed management culture, led by CEO Scott A. King, who rose through manufacturing and operational roles before assuming the top position. This background is indicative of a broader company philosophy that prioritizes execution, product knowledge, and continuity over external leadership turnover or strategic reinvention. Supporting him, CFO James C. Kerr brings financial discipline that is evident in the company’s steady deleveraging and consistent capital allocation. Overall, the management team is characterized by tenure, stability, and a strong understanding of the company’s core operations.

Culturally, GRC emphasizes long-term employee development, operational consistency, and customer focus. With an average employee tenure of approximately 12 years and no history of work stoppages, the company benefits from significant institutional knowledge and workforce stability. This stability supports its ability to deliver highly reliable and customized products, reinforcing its reputation in mission-critical applications.

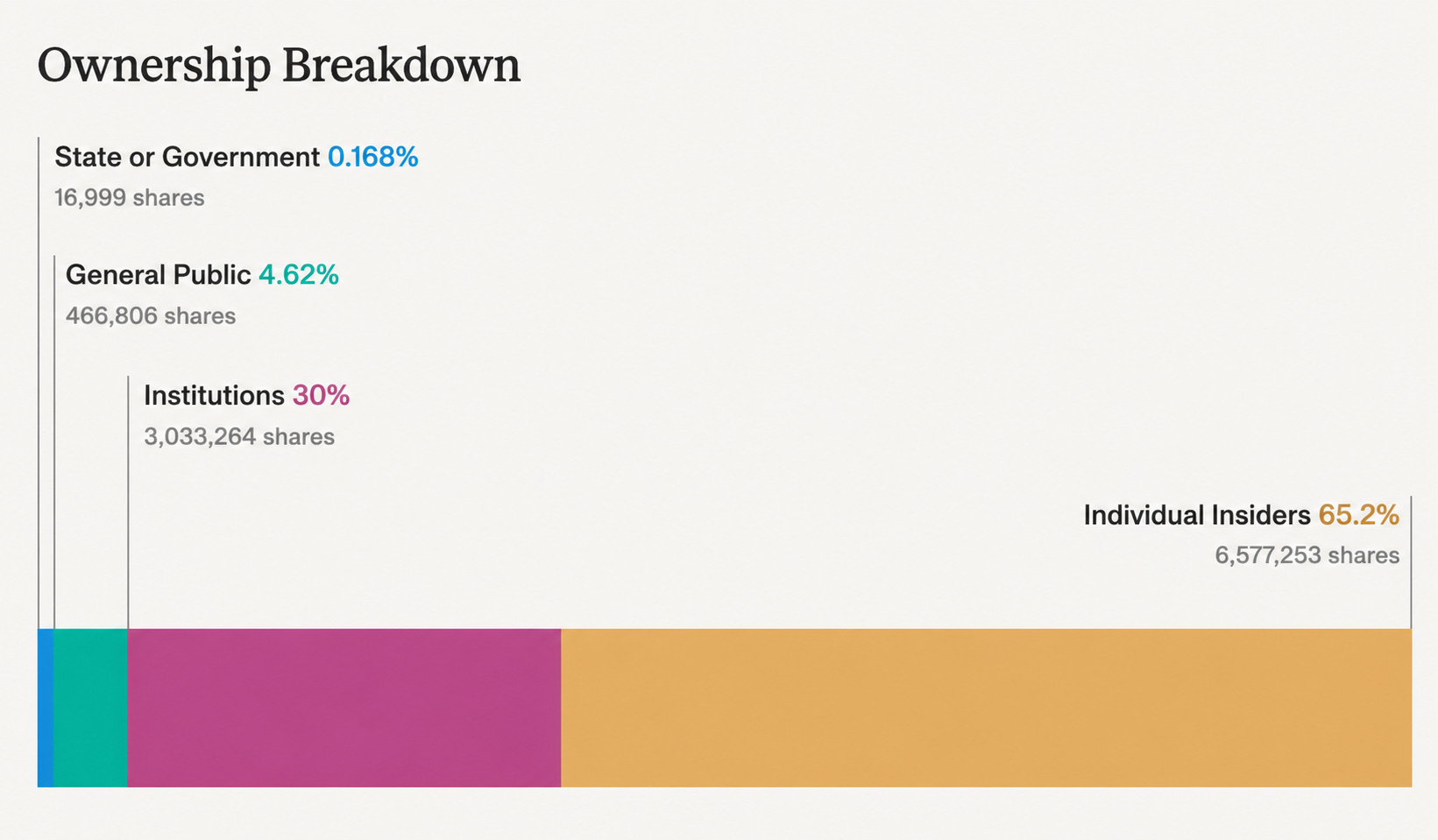

From a capital allocation perspective, management demonstrates a conservative and shareholder-aligned approach, prioritizing reinvestment, dividend growth, debt reduction, and selective acquisitions. Company’s 53-year track record of consecutive dividend increases underscores this discipline, while recent deleveraging highlights prudent financial management. Additionally, meaningful family ownership contributes to a long-term orientation, reinforcing a focus on sustainable value creation rather than short-term performance.

Financial Performance and Economics

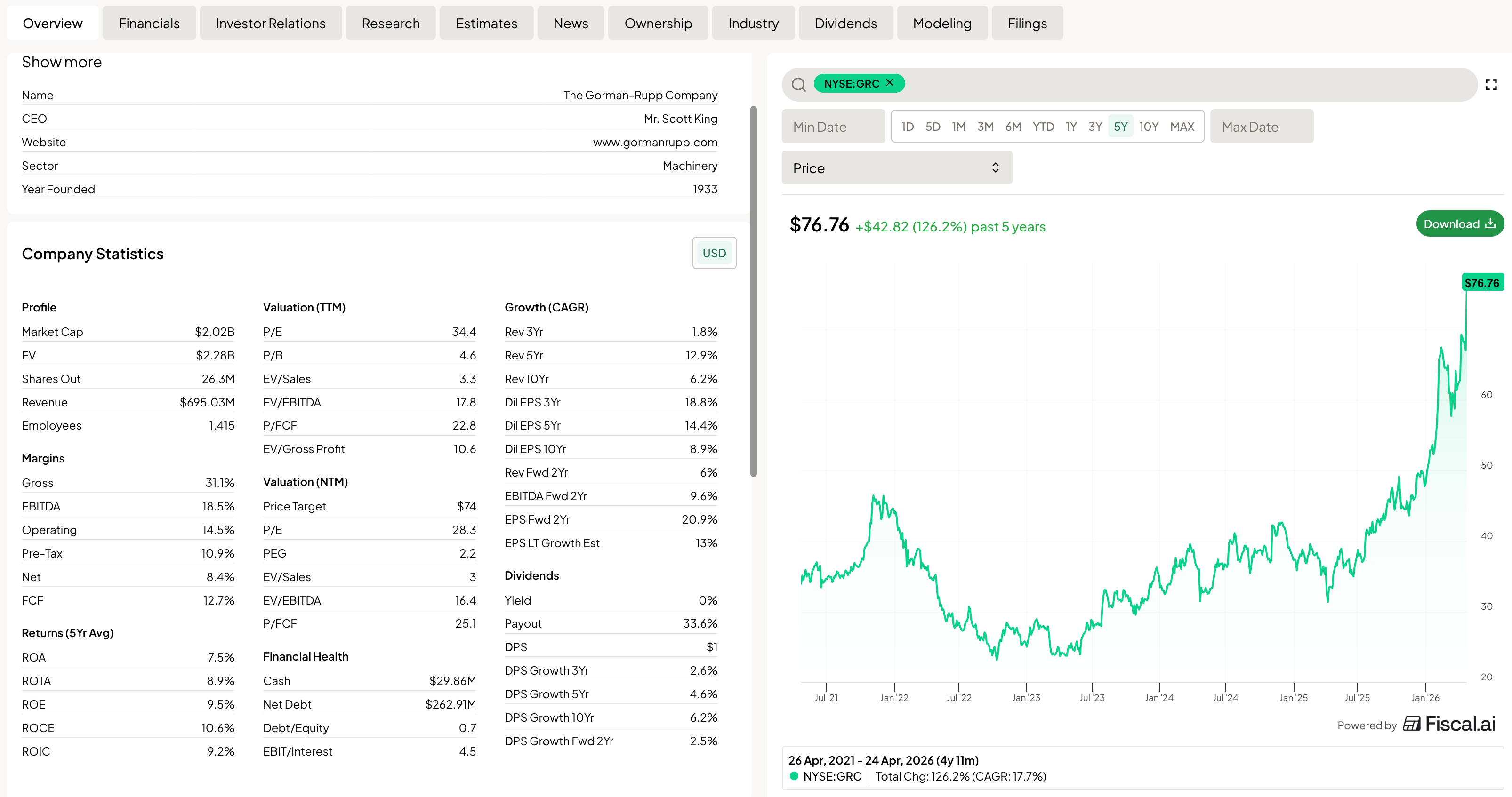

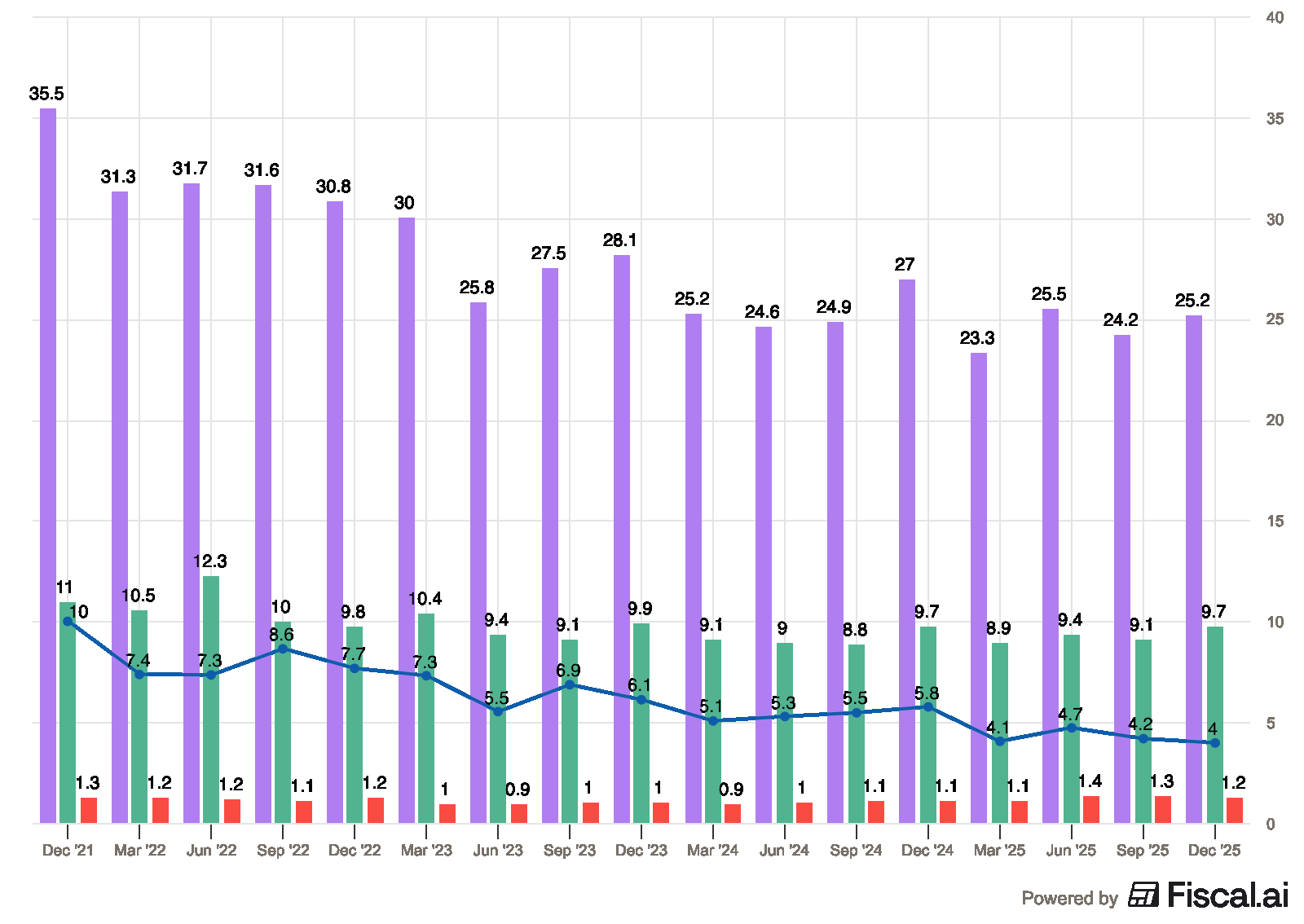

Gorman-Rupp’s recent financial performance reflects a combination of steady growth, strong margins, and improving operational efficiency. For the fiscal year ended December 31, 2025, GRC reported net sales of approximately $682.4 million, gross profit of $209.1 million, operating income of $95.4 million, and net income of $53.0 million .

Profitability remains a key strength. Gross margins reached approximately 30.6% in 2025, while EBITDA margins approached 19% . These levels are strong relative to typical industrial manufacturers and reflect pricing power, product differentiation, and the contribution of higher-margin aftermarket sales.

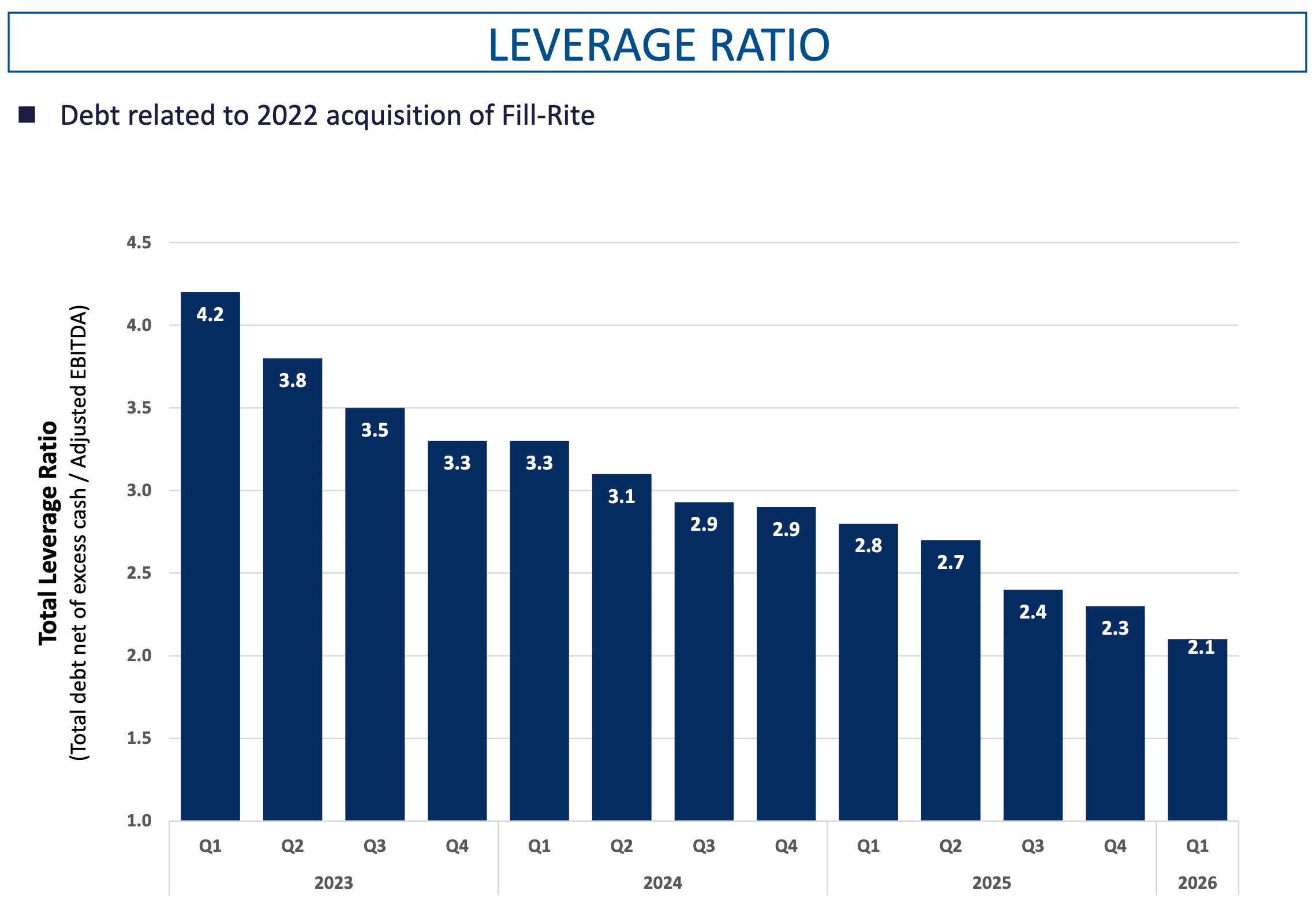

Growth has been supported by both organic expansion and acquisitions. Between 2021 and 2025, the company achieved a compound annual growth rate of approximately 14%, with organic growth contributing roughly 8ish% and acquisitions, including the Fill-Rite transaction, contributing the remainder.

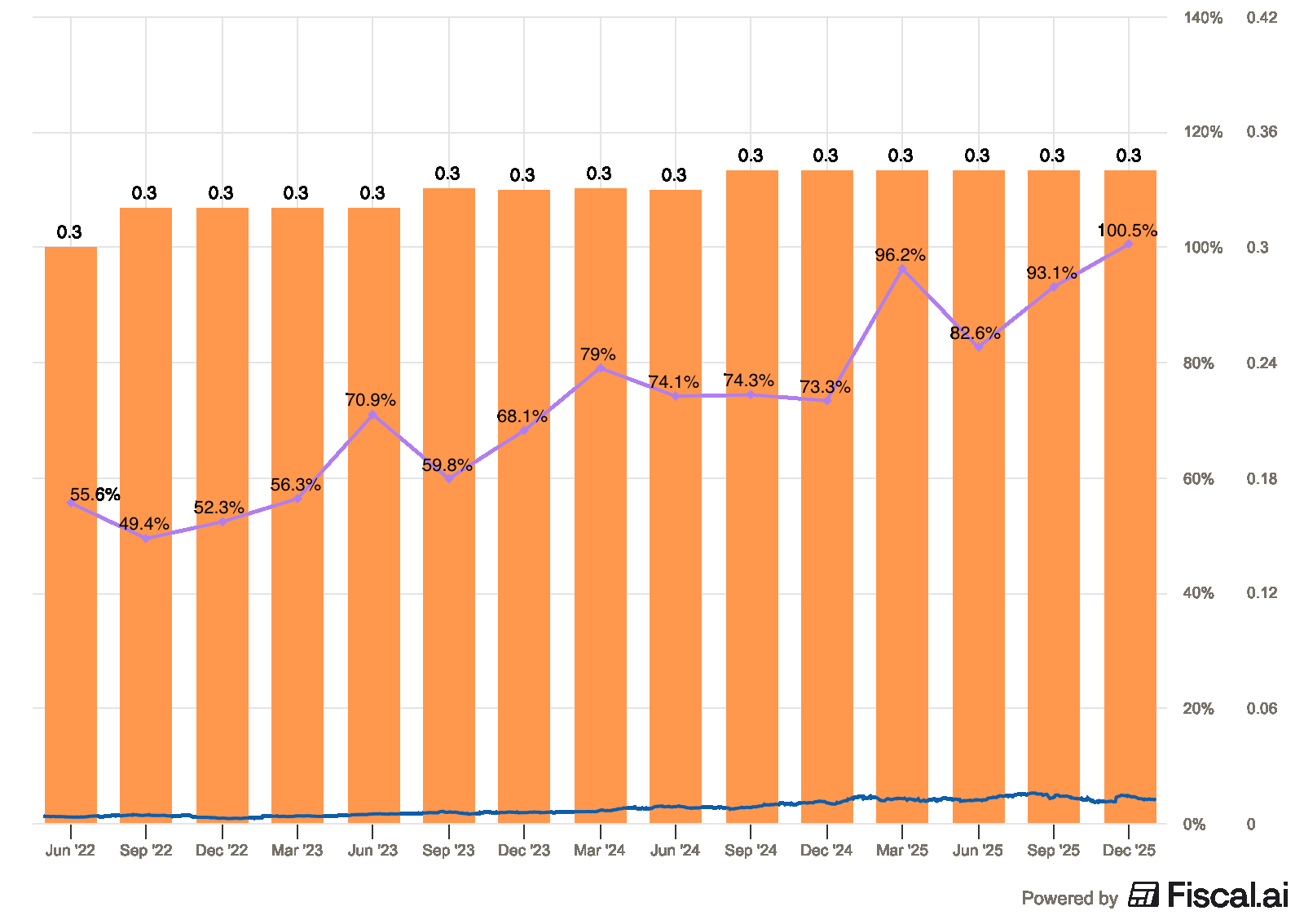

On the balance sheet, the company has made substantial progress in deleveraging. Total debt declined to approximately $310.8 million in 2025, with a leverage ratio of 2.3x, down from higher levels in prior years. This trend enhances financial flexibility and reduces risk. Management has made multiple comment on having debt reduction as one of their priority.

Competitive Landscape

Understanding GRC’s competitive position requires placing the company within the broader industrial pump value chain. This chain begins with raw material and component suppliers, progresses through manufacturing and assembly, and ultimately reaches end users through distribution, installation, and long-term service.

GRC occupies a strategic middle position within this supply chain, acting as both a manufacturer and an engineered solutions provider while maintaining deep integration with independent distributors. Company focuses on designing and assembling pump systems rather than producing all underlying components, sourcing key inputs such as motors and castings from third party suppliers. This approach allows it to remain asset-efficient while concentrating on higher-value activities such as engineering, testing, and application design.

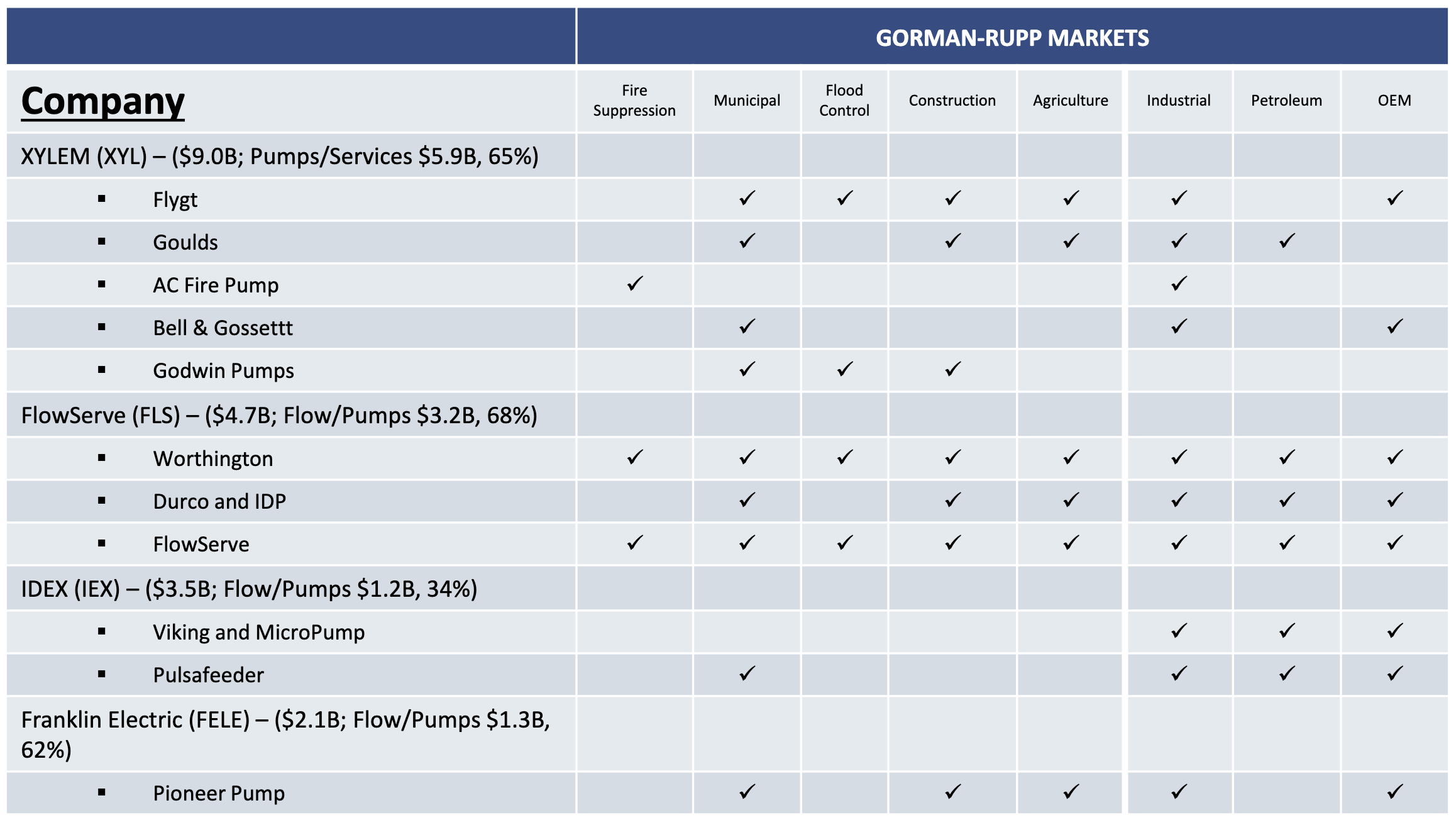

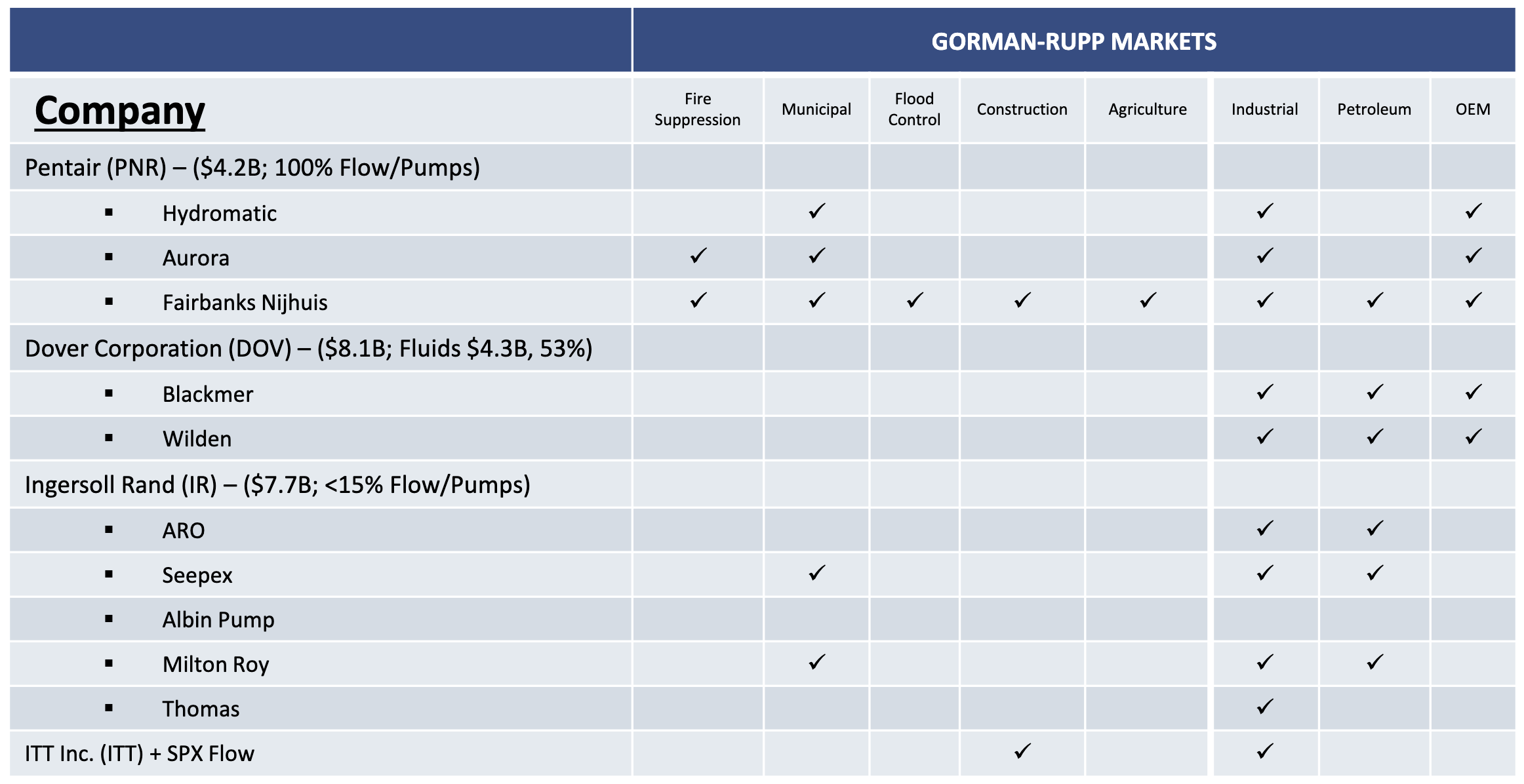

Competitors within the industry can be broadly grouped into three categories. First are large diversified industrial companies such as Xylem Inc., Flowserve Corporation, and ITT Inc. These firms operate at significantly larger scale and offer broader product portfolios, often competing in large infrastructure and global industrial projects. However, their scale can limit flexibility in highly specialized applications. GRC competes effectively in these areas by emphasizing customization, responsiveness, and strong distributor relationships rather than breadth.

The second category consists of smaller niche and privately held manufacturers. These companies often possess deep expertise in specific pump types or regional markets. GRC differentiates itself from these competitors through its combination of specialization and scale, offering a broader product portfolio, stronger brand recognition, and a global distribution network while retaining the flexibility needed to serve niche applications.

The third category includes low-cost foreign manufacturers that compete primarily on price. GRC largely avoids direct competition in this segment by focusing on mission critical applications where reliability, service, and total cost of ownership outweigh initial purchase price. Its predominantly U.S.-based manufacturing footprint further supports supply chain stability and reduces exposure to tariffs and geopolitical risks.

A critical component of GRC’s competitive positioning is its distribution network. Long-standing relationships with independent distributors provide local market access, technical expertise, and service capabilities. This network creates a localized competitive advantage that is difficult for both large global competitors and new entrants to replicate.

Taken together, GRC occupies an economically attractive position within the value chain, above commoditized component suppliers and below large system integrators. Allowing GRC to capture value through engineering differentiation, recurring aftermarket demand, and strong customer relationships without requiring excessive capital investment.

Growth Opportunities

GRC is positioned to benefit from several favorable long-term trends. Investment in aging water and wastewater infrastructure represents a significant and sustained demand driver. Increasing frequency of extreme weather events is also driving demand for flood control and stormwater management solutions.

Additionally, the expansion of data centers and artificial intelligence infrastructure is creating new applications for pumps in cooling systems and fire suppression. These emerging end markets provide incremental growth opportunities beyond the company’s traditional base.

GRC also retains the ability to grow through market share gains in a fragmented industry and through selective acquisitions that expand its product offerings and distribution capabilities.

Risks and Considerations

Despite its high-quality characteristics, The Gorman-Rupp Company remains exposed to a range of operational, financial, and structural risks that could impact performance across cycles. One of the most important considerations is the company’s exposure to cyclical end markets, particularly construction, agriculture, and certain industrial segments. Demand in these areas is closely tied to capital spending, commodity prices, and broader economic conditions. Periods of economic slowdown, reduced infrastructure investment, or declines in agricultural profitability can lead to delayed orders, lower volumes, and margin pressure. While GRC’s diversification helps mitigate this risk, it does not eliminate cyclicality entirely.

The competitive dynamics of the pump industry also require continuous investment. Market is highly competitive and includes both large multinational competitors and smaller niche manufacturers, all competing for share across various applications. Maintaining a competitive position requires ongoing spending on engineering, product development, manufacturing efficiency, and customer support. In addition, pricing pressure can emerge in more commoditized segments, particularly from lower-cost foreign competitors. If the company is unable to sustain its differentiation through performance and reliability, it could face margin compression over time.

From an operational standpoint, GRC is exposed to raw material cost volatility and supply chain risks. The production of pumps depends on inputs such as castings, steel, motors, and other components, many of which are sourced from third-party suppliers. Fluctuations in material costs, supply shortages, or disruptions in global trade can impact production timelines and profitability. While GRC has historically managed these risks effectively, including through pricing actions and sourcing flexibility, sustained inflation or supply constraints could potentially pressure margins.

Another important consideration is the company’s acquisition strategy and related integration risks. Growth in recent years has been partially driven by acquisitions, most notably the Fill-Rite transaction. While acquisitions can enhance product offerings and expand distribution capabilities, they also introduce risks related to integration, cultural alignment, and execution. Failure to realize expected synergies or operational improvements could reduce returns on invested capital and distract management from core operations. But so far GRC has proven that they are thoughtful acquirers.

Financially, although leverage has declined meaningfully, debt remains a relevant factor. The company’s outstanding debt includes term loans, revolving credit facilities, and secured notes, which introduce interest expense and financial obligations that must be serviced regardless of economic conditions. Higher interest rates or weaker operating performance could constrain financial flexibility, particularly during downturns. However, as mentioned before management has mentioned that paying down debt is one of the priorities.

Taken together, these risks do not undermine the long-term investment case but highlight the importance of evaluating GRC as a cyclical but high-quality industrial business. Its ability to navigate these risks through pricing power, diversification, operational discipline, and capital allocation will ultimately determine the consistency of its performance over time.

Conclusion

GRC represents a differentiated industrial business that combines niche specialization with scale, resulting in durable competitive advantages and strong financial performance. Its strategic position within the pump industry value chain, supported by engineering expertise, a robust distribution network, and a large installed base, enables it to generate consistent returns despite operating in a mature and fragmented market.

While not immune to economic cycles, company’s diversified end markets, recurring aftermarket revenue, and exposure to long-term infrastructure and technological trends provide a foundation for sustained performance. Combined with disciplined capital allocation and a long history of shareholder returns, GRC can be viewed as a high-quality industrial compounder with embedded recurring characteristics, capable of delivering steady value over the long term.

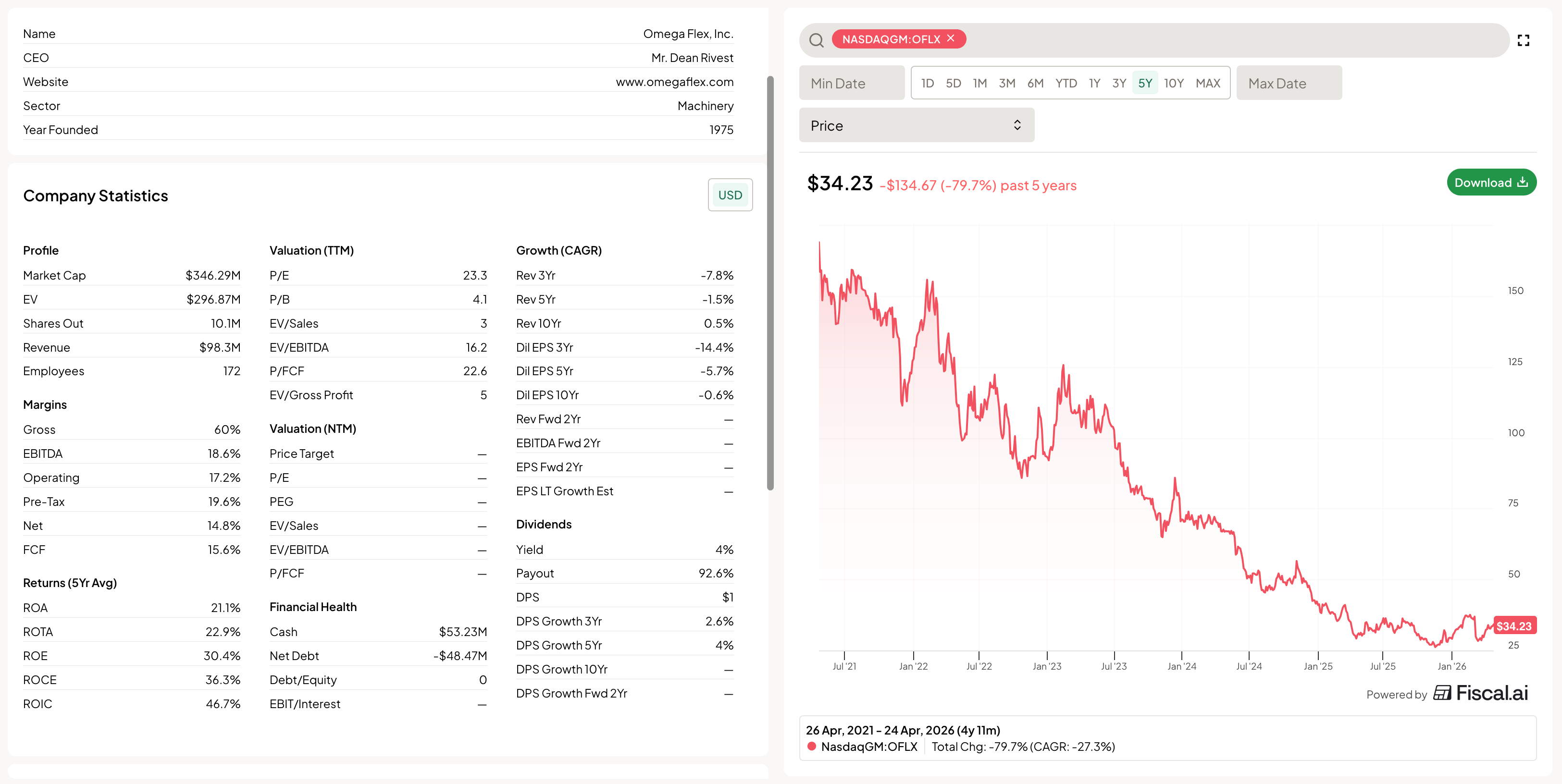

Moving on to Omega Flex, Inc. which I found accidentally by using screeners, interestingly enough there is not that much information about this company:

Omega Flex, Inc. ( OFLX 0.00%↑ )

Introduction

Omega Flex, Inc. is a niche industrial manufacturer specializing in flexible metal hose and tubing systems used to transport gases and liquids across a wide range of applications. While significantly smaller than most publicly traded industrial peers, company occupies a distinct position within the supply chain by focusing on highly engineered, safety-critical products that are primarily used in construction, energy, and industrial systems.

At a surface level, Omega Flex appears to be a straightforward small-cap manufacturing business. However, a deeper analysis reveals a company with consistently high margins, strong free cash flow generation, and a highly conservative balance sheet. These qualities are counterbalanced by limited growth prospects and a heavy reliance on cyclical end markets. The core investment question is whether Omega Flex should be viewed as a high-quality, steady cash-generating business or as a structurally constrained company facing long-term demand headwinds tied to its core markets.

Business Model and Operations

Omega Flex’s business is centered on the manufacture and sale of flexible metal hose and related accessories, which are primarily used for the safe conveyance of natural gas, propane, and other fluids. Company’s flagship products are TracPipe / CounterStrike, both are widely used in residential and commercial construction for gas piping systems while offerings such as DoubleTrac, DEF-Trac, and MediTra serve industrial, environmental, and medical applications.

Unlike more diversified industrial companies, Omega Flex concentrates on a limited number of engineered solutions, allowing it to build expertise and brand recognition in safety critical applications where reliability and regulatory compliance are essential. Its products are typically embedded within larger infrastructure systems, making them essential but not highly visible to end users. Omega Flex distributes its products primarily through wholesalers, distributors, and original equipment manufacturers rather than selling directly to end users, enabling broad market access while maintaining a relatively efficient commercial structure.

Management and Capital Allocation

Omega Flex is led by CEO Dean W. Rivest, whose leadership reflects a consistent emphasis on operational efficiency and financial conservatism. Management’s approach prioritizes profitability, cash flow generation, and balance sheet strength over aggressive expansion or acquisition-driven growth. This philosophy is evident in the company’s capital allocation decisions, which favor maintaining high liquidity and returning capital to shareholders through dividends.

Mr. Dean W. Rivest serves as Chief Executive Officer and Director at Omega Flex, Inc. since January 1, 2024 and served as its President since January 19, 2022 until December 2023. Mr. Rivest is also a director and president and chief executive officer of Flex-Trac, Director and Chairman of Omega Flex Limited and President of Omega Flex SAS. He served as an Executive Vice President of Omega Flex, Inc. since 2020 until January 19, 2022 and responsible for manufacturing and engineering for all products, as well as sales and marketing for the industrial and MediTrac’s products. Prior to that, Mr. Rivest was the Vice President and General Manager of the industrial and MediTrac’s products since 2005. Mr. Rivest is also managing director of one of the companies foreign subsidiaries. In addition to being a registered professional engineer, Mr. Rivest is the inventor of several patents directly related to it;s product lines. He served as an Executive of OmegaFlex, Inc. His credentials include an M.S. in Mechanical Engineering from Rensselaer Polytechnic Institute, a B.S. in Mechanical Engineering from Western New England College and an A.S. in Mechanical Engineering from Springfield Technical Community College.

Omega Flex has not pursued significant acquisitions or transformative strategic initiatives, instead focusing on its core competencies and maintaining a stable business model. While this approach supports financial stability and consistent returns, it also contributes to the company’s limited growth profile, as fewer resources are directed toward expansion or diversification efforts.

Industry Position and Supply Chain Role

Omega Flex occupies a specialized role within the industrial fluid-handling supply chain, functioning as a component-level supplier rather than a system-level manufacturer. Its products are integrated into broader systems such as building infrastructure and industrial equipment, positioning Omega Flex between raw material suppliers and end-market installers or system integrators.

The competitive landscape consists of both specialized hose manufacturers and larger diversified industrial firms. Omega Flex differentiates itself through product certification, regulatory compliance, and performance in safety-critical environments. This differentiation allows the company to compete more on reliability and quality than on price, particularly in applications such as gas distribution where failure risks are significant. Company’s proprietary manufacturing processes and long-standing relationships with distributors and installers further reinforce its position within its niche.

Financial Performance and Economics

Omega Flex’s financial profile reflects a business that is highly profitable but experiencing limited growth. For fiscal year 2025, company reported net sales of approximately $98 million, representing a decline of about 3% compared to the prior year. This revenue contraction was primarily driven by weaker demand conditions in construction related end markets, particularly residential housing. Operating income for the year was approximately $17 million, while net income attributable to shareholders was approximately $15 million, down from $18.0 million in the prior year.

Despite this decline, company continues to exhibit strong margin characteristics. Gross margins remained around 60%, operating margins were approximately 17%, and net margins were roughly 15%. These levels are notably high for a company of Omega Flex’s size and reflect a combination of pricing power, efficient manufacturing, and disciplined cost control. In addition, business generates strong cash flow. Operating cash flow in 2025 was approximately $17 million, while capital expenditures were modest at around $2 million, resulting in free cash flow of roughly $15 million. A significant portion of this cash is returned to shareholders through dividends, with total dividends declared in 2025 of approximately $13.7 million, or $1.36 per share.

Balance Sheet and Financial Strength

One of Omega Flex’s most compelling attributes is its exceptionally strong balance sheet. As of December 31, 2025, company held approximately $53 million in cash and cash equivalents, with total assets of about $105 million and shareholders’ equity of roughly $84 million.

Omega Flex carries no funded debt, with no borrowings outstanding under its credit facility at year-end. This debt-free position, combined with its high cash balance, provides significant financial flexibility and downside protection during economic downturns. Company’s conservative capital structure supports its ability to sustain dividend payments and navigate cyclical fluctuations in its end markets without relying on external financing.

Growth Profile and Constraints

A defining characteristic of Omega Flex is its limited growth trajectory. Over recent years, revenue has shown modest declines, largely due to cyclical weakness in construction markets and higher interest rates that have dampened housing activity. Because a significant portion of the company’s products are used in residential and commercial construction, demand is closely tied to macroeconomic conditions such as interest rates and building activity.

Company’s narrow product focus and limited international exposure, which accounts for only a small percentage of total revenue, further constrain its growth opportunities. While there is potential for incremental expansion through product innovation or penetration of niche markets such as medical gas systems, these opportunities are unlikely to materially alter company’s overall growth profile. As a result, Omega Flex does not currently exhibit the structural growth drivers typically associated with larger or more diversified industrial companies.

Risks and Considerations

Omega Flex faces several key risks, many of which stem from its concentrated business model. The most significant risk is its dependence on construction related end markets, particularly residential housing, which introduces cyclicality and sensitivity to macroeconomic conditions such as interest rates. Declines in construction activity can have a direct and immediate impact on demand for the company’s products, as evidenced by recent revenue trends.

In addition, the company’s reliance on a relatively narrow set of products increases its exposure to changes in industry dynamics, regulatory environments, and customer preferences. Long-term shifts toward electrification and reduced reliance on fossil fuels could negatively impact demand for gas piping systems, which represent a core component of Omega Flex’s business. Competitive pressures from both low-cost manufacturers and larger, better-capitalized firms may also affect pricing and margins over time.

Company is also dependent on its distribution network, with a significant portion of sales concentrated among a limited number of distributors. While the broad acceptance of its products mitigates some of this risk, changes in distributor relationships could impact sales in the short term. Additionally, Omega Flex faces ongoing exposure to product liability claims, particularly related to its gas piping systems, which could result in legal costs or reputational damage.

Conclusion

Omega Flex represents a high-quality but low-growth industrial business characterized by strong margins, consistent free cash flow generation, and a highly conservative balance sheet. Its position within the supply chain as a specialized component manufacturer allows it to generate attractive returns on capital, but also limits its scalability and long-term growth potential.

From an investment perspective, Omega Flex is best viewed as a stable, cash-generating niche industrial that offers financial resilience and income through dividends, rather than as a growth-oriented investment. The investment case ultimately depends on whether an investor prioritizes consistency and capital preservation over expansion and long-term growth potential.

Thank you for reading!

Let me know what you think about this type of short and to the point posts rather than long deep dives…

… do you like or do yo prefer long formats?

Third and fourth companies, I will be sharing in the next few days and those two will be available to the paid subscribers.

P.S. Don’t forget to ❤️ if you enjoyed it.